The movement to outcome-based services and equipment-as-a-service (EaaS) models continues. In the industrial space, organizations continue to equip themselves with digital tools and capabilities to deliver outcomes successfully. However, more needs to be done to enhance product and equipment design to deliver outcomes effectively. Organizations must also reshape their selling, marketing, financing, and servicing models and undertake a naturally daunting transformation.

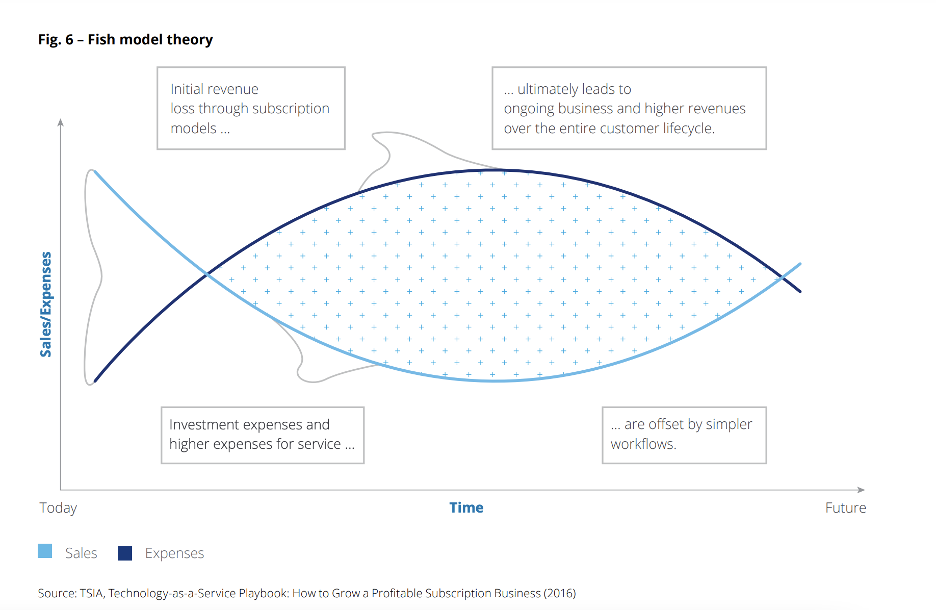

Progress continues to be slow. The decision to at least pilot outcome-based models might seem like a simple one, but business leaders have been slow to pull the trigger. The short-term loss experienced in capital revenues is hard to justify and plan for, even though the long-term impact may be more profitable. Swallowing the fish (as coined by TSIA) is a very real challenge.

Source: Deloitte. Equipment-as-a-Service: From Capex to Opex. Original Source: TSIA

When Should We Start Using Outcome-Based Models?

The decision would be a lot simpler if customers were explicitly demanding outcomes. Unfortunately, with most manufacturing organizations, we aren’t there yet. For most of our customers, a good portion of whom are evaluating outcome-based models, there isn’t an explicit demand for outcome-based services. At least not yet.

There are exceptions to this in certain industries. In aerospace & defense, we’ve all heard of the Rolls Royce power by the hour model that’s been in place since 1962. In the print and copy industry, manufacturers have been supporting ‘by the print’ engagements for some time. The proportion of their customers using these services is not extremely large, but there has been some movement in that direction.

In other industries like facilities management or medical devices, changing ownership trends are a precursor to more outcome-based models. For example, one medical device customer informed us they’d seen an increasing presence of private equity ownership over their customer labs, hospitals, and other facilities. These private equity owners were taking a more consolidated view of their purchasing patterns and beginning to demand a much more outcome-focused engagement with their manufacturing partners. As buyer profiles change in various industries, this customer-driven push for outcomes will accelerate.

While the explicit ask for outcomes might not be on the table, customers are looking to their manufacturing and service partners for several things. Most are precursors to true outcome-based models:

- Lower capital expenditures – both for the equipment, maintenance, and energy usage

- Increased reliability and uptime

- Increased risk-sharing and predictability of operations

In response, manufacturers are working on various engagement models. In some industries, organizations have moved to providing their equipment for a monthly fee, akin to a subscription or even a rental model. This means that the company does not have to buy equipment, and the manufacturer owns the equipment. However, this does not reflect a true outcome-based arrangement where they are paid based on output, quality, or Overall Equipment Effectiveness. Subscriptions are just a subset of an actual outcome-based model.

Other organizations are looking to adopt a more consumable-focused model, similar to the Gillette razor and razor blade. In these engagements, the manufacturer might sell the equipment for a low base price but look to make more revenue on consumables and materials used by the equipment. If the equipment is highly utilized to drive output, then the revenue from the use of material or consumables continues to rise. We see this extensively in packaging, high-tech manufacturing and medical devices. Once again, there is an inherent link between the use of material with better outcomes, but this isn’t a true outcome-based or as-a-service model.

We are seeing an increasing trend of customers paying for uptime-based contracts, where they are guaranteed a certain level of uptime by the manufacturer or service provider. These promises or guarantees may enable better outcomes, but there is no transaction in the level of throughput or output generated by the customer. Uptime does lead to better throughput, but the customer isn’t paying a varying degree because they produced more or less. Also, in these arrangements, the customer typically still takes ownership of the asset and has to absorb the risk associated with managing the asset’s lifecycle. In as-a-service models, the asset is typically owned by the manufacturer, who then decides when to upgrade, repair, or replace it.

[Related Reading: Refining Digital Transformation through Asset Centricity]

The Shift to Outcome-Based Services Is Slow, But It’s Coming

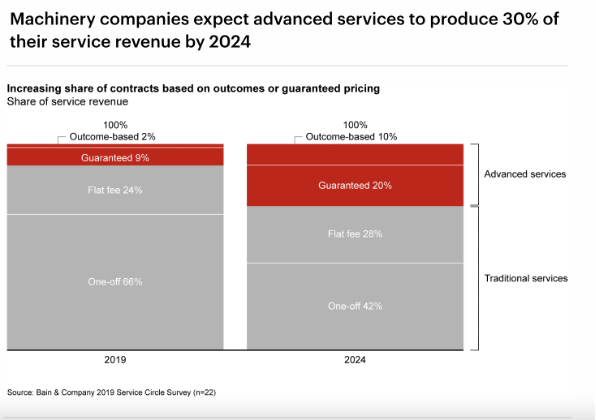

While it may seem we are splitting hairs on what is and isn’t an outcome, we can agree there is a general move towards the delivery of outcomes and the development of business models to support outcomes. New research from Bain & Company points to an increasing provision of advanced services and outcome-based models by 2024.

Source: Bain & Company, Machinery as a Service: A Radical Shift is Underway

The numbers don’t necessarily jump off the page or highlight a radical shift. That’s the point. This shift is slow, but customers are beginning to lay the groundwork for their interest in outcomes. Manufacturers can either wait till those requests become explicit demands or can start proactively supporting their customers’ ambitions of better outcomes.

Share this: